I am writing after a full month and owe it to myself and everyone who might read why there was a gap. I set myself goals and just fell short. So, here is the roundup, what I failed to do and how I am planning to avoid a repeat.

Tennis – The New Horizon

As it stands, I know what my money is. It is a single source. I did extract more from it and now, I will be writing on tennis in addition to football. This is a welcomed addition and I want to make the most from the opportunity that provided itself.

This was the good news. There were some setbacks as well. For the last nine months, I took on a daily task and diligent in performing it. It also meant that I would be pocketing $300 from the twenty minutes I put in every day.

But we all make mistakes and I did too. One late night, I messed up the dates and published the wrong article. I slept in late and by the time I responded to the messages, it was late. One part of the daily tasks was taken from me.

I explained myself but was told not to work on that assignment anymore. To tell you the truth, I did not take that in the right way. My knee-jerk reaction was to absolve myself of the other publishing task as well. And I did so.

Now, I was in a $300 hole and needed to fill it up. Fortunately, the tennis role opened up and I helped myself to it. So, I am still at the same level where I started but the good thing is, I am widening my area of work, which should help in the long run.

Finding Real Work in Germany

I failed at this task miserably. It was shambolic to say the least.

I started looking for a job, one in which I will have to leave my house every day. I was willing to make less money but it was something with a long-term goal.

And one such opportunity came. My brother hooked me up at his workplace and it was in line with what I wanted. An accounting role which can be transitioned into taxation. That was the goal at least.

I had recently been looking at ATT UK and this would have been a great role to learn the ins and outs. But it was not meant to be. I gave a couple of interviews but did not impress the hiring people.

I did not share it with anyone but it really hurt me. And I got into my shell. This happened right when I was also relieved of the daily publishing tasks I mentioned earlier. So, the couple of setbacks resulted in me doing nothing and just wasting time.

I have not gotten back into the fold since and really had to force myself into accepting this. It is easy to say that there are other fish in the sea but when you think you are close to achieving a goal and do not, getting back on track is not easy.

The Way Forward

I was knocked down but not out. That’s why I am writing this entry.

To move forward, I have set myself three goals for my journey.

First, I will work on the website for one hour every day. If I write content every day. If I do not have the motivation to write, I will work on the outlook and other factors that affect the website. But I will do something on Finanzen404 every day.

Secondly, I will set aside one hour daily to learn something. This is the minimum I will do. I have two skill targets in mind. Technical Writing and Email Marketing are the focus of my attention. The first will help me write about software that can be useful in my journey. The other will help me make an email list so that people can get my emails in their inboxes.

Third and most important, I will become active in searching for a job. I will search for jobs for thirty minutes and then get to other tasks. It might increase but with constant effort and as my portfolio grows, I should be able to complete this task.

Learning about finances is not included in these tasks. That goes without saying. That’s the ultimate goal and with these actions, I plan on achieving it.

In my last post, I laid down the gauntlet. I said it out aloud. I am not going to lie. It was overwhelming and I got scared writing it all. The more difficult part was clicking the publish button.

Everything that could go wrong went through my mind. I made note of all the different what-ifs as they raced through in front of my eyes. I think it all boils down to accountability. If I put it out there, I will have to live up to it. And if I fail, I will be a social pariah.

It did not stop me. I realized, no one will read this. Its a new website and probably not even indexed in Google. I will get to that part in a couple of weeks if I am publishing regularly. See, I have a backup plan already. Hate the pessimist in me.

I published what my goal is going to be, so what’s next? I need to own my money now.

Who Owns My Money Stream

Before I can get to saving and investing or starting a business, I need to know money, my money. The roads in front of me will only open I am aware of where I am exactly.

So, a little more introduction about myself. I am a Sports Blogger turned Communication Professional turned Business Analyst turned Freelance Data Analyst turned Sports Blogger.

Money has usually been tight for me. I returned to writing for sports as it was lucrative, and the exchange rate from USD to Pakistani Rupee made the decision easier.

I have been at it since June 2021. I liked doing it initially but not anymore. And I know AI is coming for my job. It pays the bills and I am happy about it. So, I cannot complain.

But it is a freelance contract. The employers are nice but they are also doing business. They have no loyalty to me, it is to their objectives. And since I have been made redundant before, I cannot allow them to be the sole providers of my money.

What Are the Other Money Streams

I am a freelancer with just one client. This is bad. Again, as I type this out, I realize how big a problem it can be. I cannot rely on this source of income alone.

So, I need to find other sources of income. What are the options that I have.

Find another client

Start a business

Temporary jobs

Ask the current employer for more work

To be safe, I should start searching for a new client. That should be my first target. I found the current client thanks to cold emailing. I will have to go through the same routine again.

I know I should have done this a year ago but I succumbed to Newton’s third law and enjoyed comfort far too much.

About starting a business, I do not think I can do that right now. Far too timid at the moment. But this is where you all come, my invisible audience. I want you to spur me on.

A temporary job is not an answer right now as well. I am not at risk of losing my job and have saved for around three months. If shit hits the fan, I will be of to the races for it. I will be cycling around Munich to do that. But first, I have to find a new contract.

A fourth option can be asking my employer for more work. I can save money or possibly retrain in some other field. That can help in the long run as well. And if nothing, I can improve my conversation for seeking work. Fingers crossed.

My Streams Are Running Dry

Football is life.

Dani Rojas – Ted Lasso

I love football and writing about it makes me nauseous about the game. I want to watch the games but do not want to put in the extra effort to even turn on the television. It makes me think about work. And I just don’t go through with it then.

The bigger issue is that I am at the same level that I started at. My skill level has deteriorated and with good reason. I only write on this one subject and for one specific reason. And I am not helped in any way to improve this: no stats provided, no data shared. They can fire me in the next instant and replace me with a monkey who can type. And there will be no difference.

So, it’s time to move away. I need to find another source of income. I have been doing Hubspot’s Digitial Marketing certification and can put it to use. I seriously need to think about my career and whether I should change it or not. I have 30 good years of working left in me and I want to make the most of it.

Takeaways From the Second Session

I realized that my income source is a vulnerability and I need to address it. My money tap can be switched off with one sto

While I increase my financial knowledge, I need to diversify my sources of income. Finding another client is top priority, which is closely followed by asking for more work. Will update my plans and activities on this front later.

I am realizing that I am making some very bold statements in these blog posts. It’s like talking to my inner voice. I make these promises in my head as well. But there are more people there. That’s a discussion for some other day, so we will get into it later.

Salutations to anyone who is reading. Like everyone else, I like to have money. Be carefree about it. And like most of people on this planet, I do not have it.

At the age of 36, I realized I need to take action for this. I need to have a plan for achieving this. I will be 50 soon and that part of life goes like a breeze, so I have been told. And then the 60s hit you. That’s the descent into the 70s and senility.

I have no plan. My job will be overtaken by robots soon. I earn too little. And the 40-year journey to million dollars and beyond is not in my reach. I have to buy a home sooner rather than later. Will have kids soon, so that’s expensive. Nothing in my life is going according to any plan.

The goal is set. It has been set for quite some time but life just keeps on happening. And I have been going with its flow.

As I write this, I realize that I need to be accountable. It will be key to my success. This is why I explicitly sat down and started writing. And as all my thoughts wander in my mind, it is the one defining factor. Alongside, having a comprehensive plan to follow through.

Like most people around, I do not have anyone to talk to. I am distrustful of financial planners. Not because they are out there to get me and want my money. But for two reasons. I am embarrassed by my situation and I am fearful of asking for help. The feeling of being dumb is overwhelming.

Google Will Tell You to Actively Save and Invest

So, like everyone who is scared of asking for help, I did what everyone else does. I asked Google to help me. It was a waste of energy and time. I came across 6000-word articles that were just generic advice.

And it all boiled down to one thing. No, roadmap whatsoever. I wanted someone to hold my hand and show me the path. And I did not want to pay anyone. It did not go according to my plan.

Anything that you will come across will be centred around saving this much for this many years and you will be a millionaire.

How does this help? I know compound interest is very powerful but it seems just a way to pour money in savings depots and earn affiliate commissions for these content creators.

But this is where their help finishes. I have no qualms with affiliate marketing, I would profit from such an opportunity too. But also guide the audience in making the right investments.

I like this advice but I also believe this is not the only way. It is one way of going about it but it is a very passive way. I want to be accountable. I want to be the master of my own journey and be active in my approach.

Actively saving and investing that amount is a very respectable approach. Especially, if you have all the burdens of the world, from going to work to taking care of the family and just want to take care of your portfolio.

But this only works if I would have started early. Or have decent savings. Or knew how to find the right investment stocks and ETFs or Index funds.

But it cannot be the be-all and end of all of becoming a millionaire. And surely, it cannot be the only way to achieve this goal.

The One Youtube Video You Should Watch

I was planning for my life and I got bored of reading the same advice in different packages on Google’s first page. All it took was an hour.

But I could not give up and my idea of an active path to millionaire status brought me to YouTube. It did not go well.

First, I cleansed my mind and watched random videos. It was one of these days, I had a plan and YouTube had another.

But after a couple of hours, I am not joking here. After spending more time watching YouTube videos than reading about my 10-year plan, I forced myself to make the search.

I knew the same material would be regurgitated there. And millionaire creators did not disappoint. And then I came to Anthony Vicino’s video. It resonated with me and it should with you as well. I have embedded it here and would ask you to give it a watch as well.

Budgeting Is Important and so Is Knowing Your Money

Advice over the internet, be it YouTube videos or financial management blogs, is unanimous on two key pieces of advice.

The first is that we need to start saving and put that money to earn more money by investing it.

The second is that I need to know my Money. I need to know where it is coming from, how much it is and how it is spent.

It may sound easy for most of you but for someone on a freelance contract, it is difficult to ascertain it exactly.

Moreover, it becomes more difficult if you are nonchalant about your money. If you are like me and spend money knowing more will come, you are in for a rude awakening.

Anyways, I need to look into it in detail. It is not just knowing where I spend it but also knowing the thought process.

Takeaways From the First Session

It is going to be very BORING. And DIFFICULT. And TIME-CONSUMING.

It is a jungle out there and too much information. There is so much to learn and will require effort.

I need a concrete plan. But I cannot make one without knowing my finances, and my future goals. I cannot just think I am going to be a millionaire in 10 years and it will magically happen. It is just the first step.

It is daunting to know that half of your life has passed but you are still on the first step. But one thing that every writer and influencer told me was that there is still time. It is never too late.

For whatever are their reasons, I want to be optimistic in my approach. And they might actually be genuine in their advice.

So, here it is. I will be optimistic in my approach and actively craft my roadmap.

For anyone wondering why I wrote this, it is simple. It is frustrating to find an answer. And I did not find an answer. I got clues to build upon. You might find yourself in a similar situation. Don’t get discouraged. Soldier on.

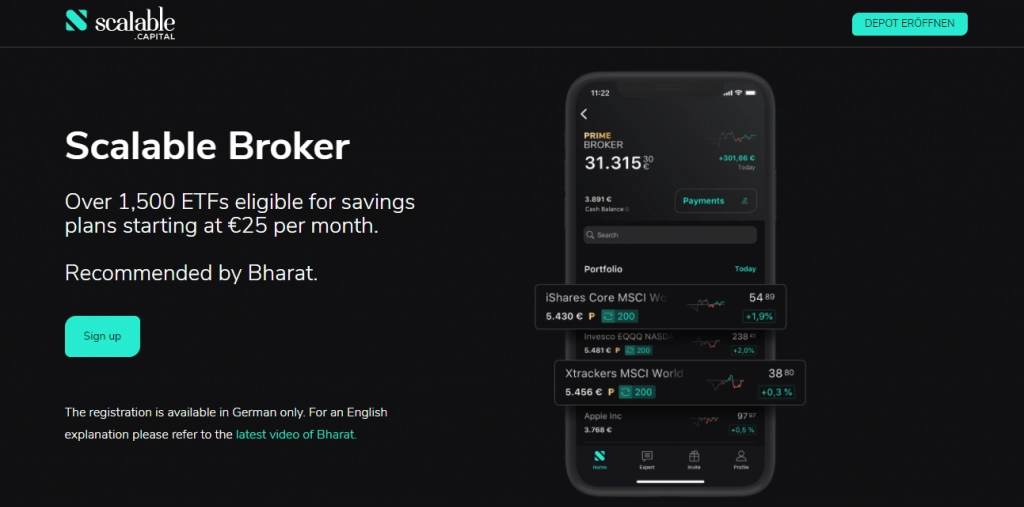

If you want to invest in stocks, options, and ETFs, you need a Depot or depository account and Scalable Capital provides you with ease.

So, without waiting, let’s get started with opening an account with Scalable Capital!

Who Can Sign up for Scalable Capital?

Scalable Capital’s services are aimed at individuals residing in Germany, Austria, Italy, Spain, France and the Netherlands. In addition, the following requirements must be met:

You should be over 18 years of age

The US tax jurisdiction does not apply to you

You are not a Swiss resident

You have a SEPA current account

Note, however, that the custodian bank only pays taxes on the customer’s behalf if they are taxable in Germany. If you are subject to tax outside of Germany, you must make sure that all securities transactions are taxed properly. For these reasons, Scalable Capital will provide you with a tax report.

Opening a Depot With Scalable Capital. How to Get Started?

Scalable Capital has made the process very simple to sign-up for an account and can be concluded in five simple steps

Go to Scalable Capital’s website and tap/click on the “Open Account” button. Sign up with your email address.

After signing up and verifying with your email, select a Broker Plan. Go with a free plan to straighten your bearings.

Fill out your personal information

Make your first deposit

Verify your identity.

Let’s take a look at these steps in greater details.

Step 1: Signing up for Scalable Capital Using Your Email ID

Go to Scalable Capital’s website and click on “Open Account“. We have made this process simpler for you, so go ahead and click the link above or the button below.

You will have two options. If you want to manage everything on your own, select the Broker option. It is available in English and German language. Select Wealth option, to invest in a portfolio that is managed by Scalable Capital.

Both options will redirect you to a webpage where you sign up with your Email Address. Scalable Capital will send you a verification email, which you need to follow to get to the next step.

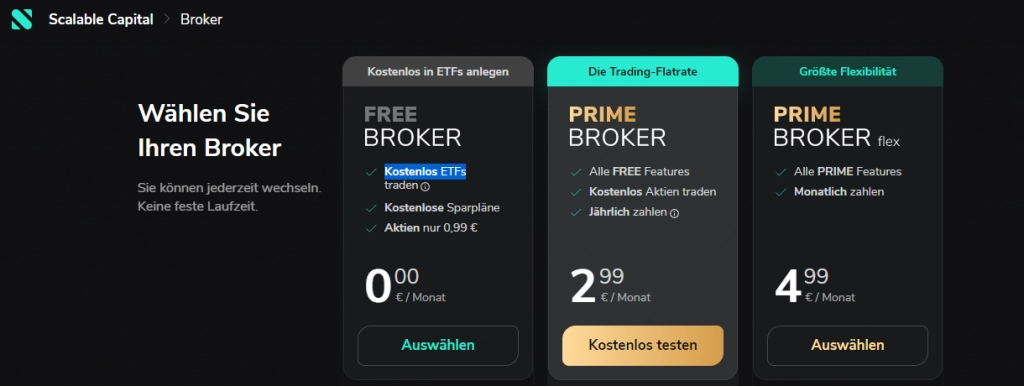

Step 2: Choose the Broker Plan of Your Choice

After you verify your email address, you will be taken to a brokerage plan page. Choose a broker plan for your depot according to your needs. You need to select one of the three plans offered by Scalable Capital: Free, Prime or Prime Flex. Each plan has different features and fees.

A) FREE Broker Plan

The Free Broker Plan does not incur monthly subscription fees. When you open a free ETF Savings Plan and invest in Scalable Capital’s PRIME PARTNER ETFs, transactions are free.

This plan allows you to trade over 4,000 ETFs and funds for free, as well as trades with an order volume of €250 or more in selected products from Invesco, iShares by BlackRock and DWS Xtrackers. The minimum amount for a savings plan starts at €25. For all other trades on Gettex, you pay €0.99 per trade. Crypto ETPs are subject to an additional spread surcharge.

These can be summarised as:

No order fees for ETFs

Fixed order fees of €0.99 for shares

No account management fees

B) PRIME Broker Plan

The PRIME Broker Plan costs €2.99 per month. In addition to everything in the Free Broker Plan, it also gives you unlimited free trades for all products on Gettex, including stocks, ETFs, funds and crypto ETPs. You also get access to exclusive features such as fractional shares, smart order routing and best execution. This is actually a great advantage since it opens you up to so many options.

These can be summarised as:

No order fees for ETFs

No order fees for Shares

No order fees for derivatives

Monthly account fee of € 2.99 per month.

This is an annual subscription, which means you will pay for the whole year at the time of signing up or upgrading your account from Free Broker Depot.

C) PRIME Flex Broker Plan

The Prime Flex plan is an upgrade to the Prime plan. This plan costs €4.99 per month and gives you all the benefits of PRIME Broker plus unlimited free trades on Xetra (Germany’s largest stock exchange) for selected products from Invesco, iShares by BlackRock and DWS Xtrackers. In contrast to the PRIME Broker plan, payments for PRIME Flex are monthly.

These can be summarised as:

No order fees for ETFs

No order fees for Shares

No order fees for derivatives

Monthly account fee of €4.99 per month.

Unlike Prime Broker, Prime Flex Broker has a monthly subscription. It means you will not be charged for the whole year but on a rolling basis per month.

What Is the Difference Between Gettex and Xetra

Gettex and Xetra are both electronic trading platforms for securities in Germany. However, they have some differences:

Xetra is the largest exchange centre in Germany by far: around 90 per cent of the sales are attributable to this platform. Gettex is a lot smaller and predominantly caters to private investors.

Most of the trading at Gettex takes place with so-called market makers, who provide liquidity and competitive prices. Whereas Xetra is a pure stock exchange that matches buyers and sellers directly.

The trading hours of Gettex are from 8:00 to 22:00 CET, while Xetra operates from 9:00 to 17:30 CET.

Step 3: Add Your Personal Information

Once you choose your plan, you will be taken to a page where you need to fill out your Personal information.

Name

Title

Marital status

Citizenship

Address

Tax Number

IBAN Number.

Why Is This Information Required?

European Union and German regulations, including the Money Laundering Act, mandate Scalable Capital to verify customers’ identities. To comply, the data is collected during account opening. Nevertheless, it is kept private and not shared with any third-party organizations.

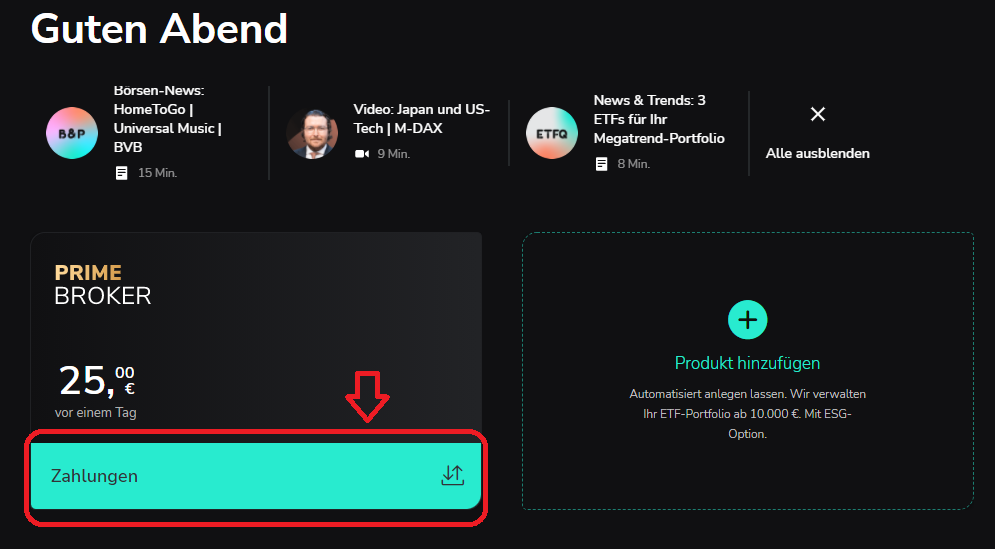

Step 4: Make Your First Deposit With Scalable Capital

Scalable Capital’s depositing process is fast and easy. You can use Direct Debit or Bank Transfer to make your payment. The type of account you select may require additional verification before making a deposit.

For new investors, starting with a small amount is better. A minimum investment would be €25, since it is the least required for a savings plan.

You can initiate a deposit via Scalable Capital’s web customer area or through the ScalableCap app. This is what the customer area looks like from the web login:

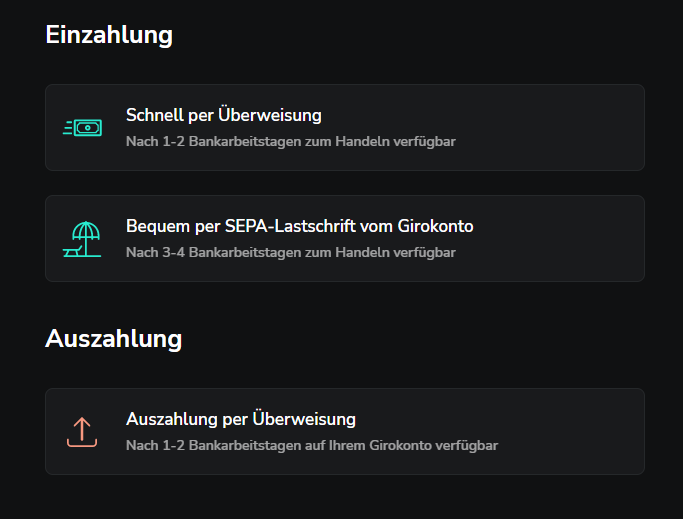

You can use the menu item to choose between two options for paying money to the clearing account:

Deposit by bank transfer (1 to 2 working days)

SEPA direct debit (3 to 4 bank working days)

Deposit by Bank Transfer

If you choose this option, the IBAN of Scalable Capital’s clearing account at Baader Bank will be displayed. You can transfer any amount from your own checking account to the clearing account.

To simplify the process, a QR code will be provided. You can scan it with your banking app and be on your way.

Your money will be in your account within 1-2 working days.

Please note that the checking account should be in your name or the transfer will not go through. Moreover, transfers via PayPal, Payback and Wise are not accepted.

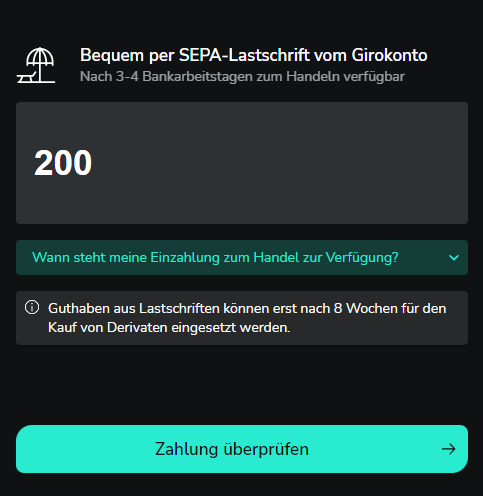

SEPA Direct Debit

The more easy way is to deposit by SEPA direct debit as you do not have to leave Scalable Capital’s environment. The image below shows how you can access it directly in the client area.

To use this option, you have to deposit at least €100. Moreover, you will have to wait longer as it will take 3 to 4 working days for the money to appear in your account. It takes longer as your bank has to confirm the direct debit.

If you plan on investing in derivatives, you will have to wait for up to 8 weeks.

Remember, always check all the information you have entered thoroughly before moving to the next step.

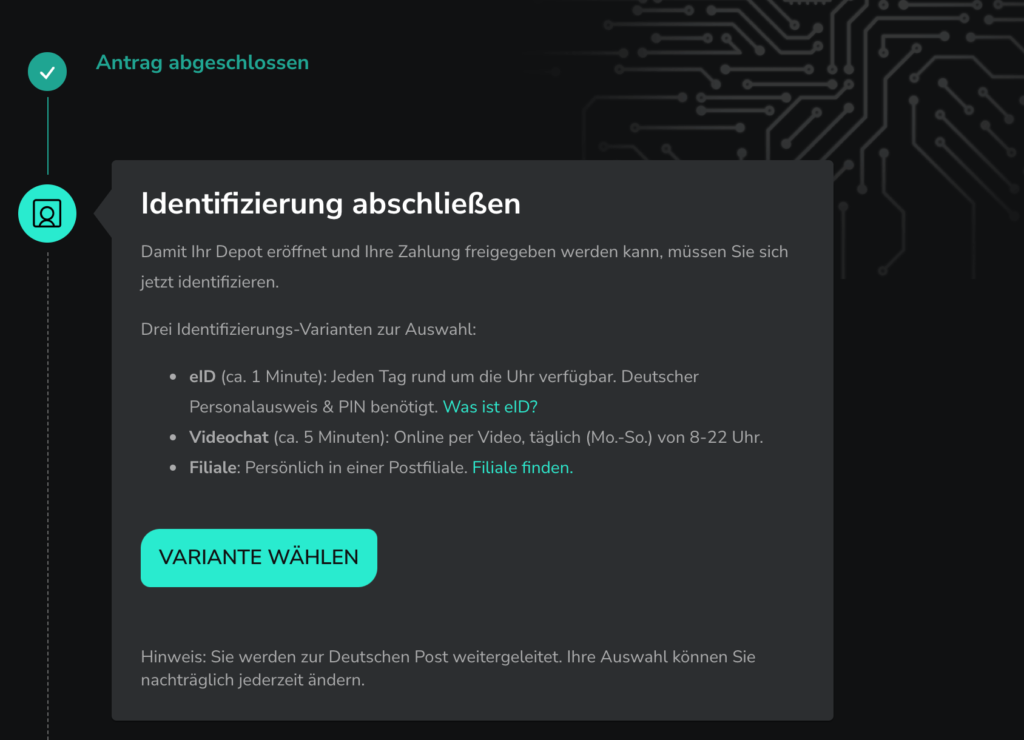

Step 5: Verify Your Identity WIth POSTIDENT

After agreeing to the Terms and Conditions, you will be directed to the Identity Verification stage. Scalable Capital has partnered with POSTIDENT to securely verify your identity.

There are three ways to verify your identity:

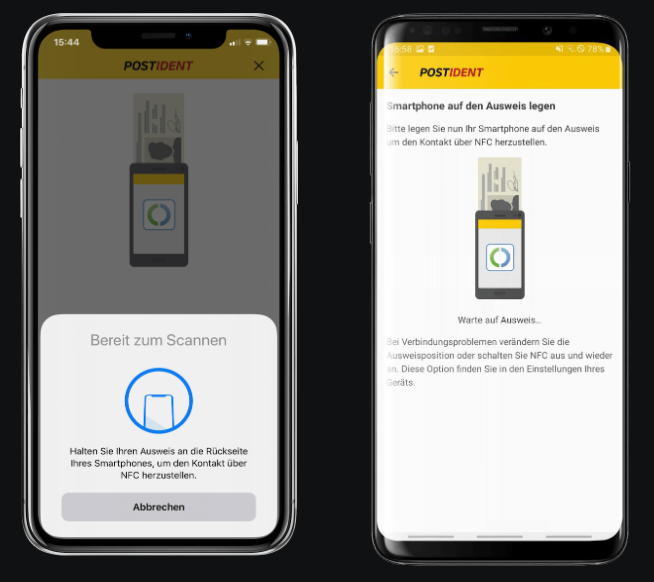

1. Verify With the POSTIDENT App

All you need is your German residency card and you can get verified within seconds, let alone minutes. You can also use your driver’s license issued by a German body to get verified. Just download the POSTIDENT app, scan your card, and you are verified.

2. Verify Identity Online by Video

If you have a foreign identity or passport, you can verify through this option. Have your passport nearby and follow the steps. You will be asked to hold it next to your face, so make sure there is enough lighting.

3. Identification in-Person at a Post Office Branch

If you cannot verify through video, you will be forced to make a trip to the nearest post office. They will scan your document and probably also take your fingerprints. It is easier than it sounds.

Once the verification is complete, you are all set. There is nothing more to follow upon. In a couple of days, your deposit will be completed and you can use Scalable Capital.

Life insurance is an essential part of financial planning and in Germany, it is no different. It protects your loved ones from financial hardship in case of your death and helps fund their retirement. It allows you to plan for your own future or provide for a special project, such as buying a new car or getting married.

Life insurance can also be used to pay off debts like mortgages, loans and credit card bills so that nothing falls on your family’s shoulders if something happens to you unexpectedly.

What is German Life Insurance?

Life insurance policy will ensure upon the death of the insured person that a selected sum of money is paid to his or her dependents. This payment amount is determined by the insured person’s age and medical history, as well as other factors.

The life insurance policy can be taken out either in a single sum or in instalments over time. The latter option allows flexibility and helps getting your money back if you need it during the course of your life.

If you have dependents who rely on your financial support or if you have taken out a loan that needs to be paid off, life insurance in Germany assures that the lack of income caused by death will be compensated.

Who Needs Life Insurance in Germany?

Life insurance isn’t just for older people–it’s something everyone should consider having in place before it’s too late!

If you have people who are financially dependent on you, then it is wise to consider purchasing a life insurance policy. Alternatively, if your income allows others to live comfortably without depending on it—e.g., an elderly parent living off of retirement savings or Social Security benefits–then there is no need for at least this form of life insurance in Germany.

Many adults consider purchasing life insurance once they become parents—because a child’s well-being is directly tied to the family’s income. But some couples might not need additional coverage if their savings could comfortably support them in the event of one spouse’s death, or the other can still earn an income.

You should consider life insurance if you fall into one or more of the following groups:

Parents with children. If you have dependents, it may be necessary to take out a life insurance policy large enough to cover their needs in the event of your death. Coverage will help pay for food, clothing, and other household expenses—such as daycare assistance and tutoring when needed by your kids. If your children are older (or have left the house), you may only need coverage until they enter the labour market/#ENDWRITE

Primary breadwinners. If you are the main earner in your family, life insurance can provide financial protection for your spouse if you die and they have difficulty making ends meet.

Self-employed/Businessmen. Life insurance can provide the necessary funds to keep a company running if its owner dies or becomes disabled.

Old People. In some cases, older adults may not have savings to pay for their funeral expenses. In this case, you will need a life insurance policy large enough to cover the cost of your own burial or cremation in order that family members do not incur these costs themselves.

Adults with (student) loans. Life insurance can be used to pay off a deceased person’s debt, including student loans.

Financial experts say that life insurance is a valuable type of insurance for anyone who financially supports another person, whether it’s their spouse or children. And even if you do have dependents, life insurance should only be purchased to see out the time that allows you to support your family financially.

What does life insurance provide?

Term life insurance is the most affordable type of life insurance and can be used to pay off debts, such as student loans. It provides a financial safety net for your family or other surviving dependents and can serve as collateral for loans, such as mortgages.

Beneficiaries can be anyone, not just family members. Your dependents will get the insurance payout even if you only started paying premiums a short time before your death. However, the policy will only pay out if the insured event occurs during the term of insurance.

When you take out a life insurance policy, the insurer promises to pay your beneficiaries or estate (the people who will receive the money) if something happens to you. Term life insurance does not build up capital like the policies sold for endowments do.

As a result, premiums are considerably lower than those paid by someone with an endowment policy—though you should still make sure that your monthly payments will not be too high to cover all of your other bills.

If the insured person survives past the agreed-upon term of their policy, they do not receive an insurance benefit. Their premiums are also not reimbursed because the insurer has been bearing all of that risk—the agreement is simply over at that point. It’s like cancelling your gym membership when you start to lose weight: if your goal is accomplished before a specified date then no refunds will be made and there’s nothing more to talk about.

Pleae note that if a person takes out insurance on the life of someone else, that is if the insured and policyholder are not the same person—the insured must give their written consent before policies under certain conditions become effective.

What are my obligations as the policyholder or insured person?

Paying the premiums on time and in full. If you don’t pay premiums, your policy will lapse and any benefits paid out will not be refunded.

Notifying your insurer of any changes to your health status (e.g., if you are diagnosed with a terminal illness) so that they can adjust the premium accordingly.

You might also be subject to additional obligations, so you should carefully read your insurer’s general terms and conditions for term life insurance (Allgemeine Bedingungen für die Risikolebensversicherung).

How Does Life Insurance in Germany Work?

If the person who has a life insurance policy dies, the life insurance company will pay a particular amount of money to the dependents (which are assigned by the insured person the moment they signed the contract).

With this amount, the family will be able to support dependents, maintain their expenses, and pay the insured person’s loan. Apart from helping to support dependents, life insurance will also be of help when it comes to immediate cash or funeral expenses.

How to Get Life Insurance in Germany?

The process of getting life insurance in Germany is not as complicated as it may sound. You can get a quote from a provider online, over the phone or at your local branch office. If you already have an existing policy, all you need to do is make sure that it’s still valid and up-to-date.

The first step before getting life insurance is to figure out what kind of coverage your family would need if something happened to you.

You should consider what the costs will be in a worst-case scenario, such as immediate funeral and medical bills. Taxes can also factor into your planning calculations long before you die; if you don’t take them into account now, it could impact your financial plans for retirement down the road. Moreover, you should take into account long-term expenses like college tuition, debt payments, and retirement funds.

You may purchase life insurance online, by phone, or in person (by visiting a company’s branch). An insurance application will ask you to provide specific documents, personal IDs, bank statements, list the beneficiaries, and ask a set of questions related to your circumstances (spouse, children, debts, mortgage, health, hobbies, etc

How to buy life insurance online in Germany

Tips to buy life insurance online in Germany:

Finding a life insurance company that suits your needs. You can purchase life insurance from a wide variety of life insurance providers in Germany. You’ll need to choose which one best suits your needs and finances.

Answer a series of questions. You’ll need to go to the chosen provider’s website and select the type of life insurance you need after selecting your provider. Questions may be regarding your health, whether you are a smoker or not, your family’s health, your job, whether it includes dangerous activities, your lifestyle, and many more.

Decide how much insurance you require. In the event of death, you should determine how much money your dependents would need. Funeral costs, debts, future costs, etc are taken into account when deciding on your total needs.

Specify the contract length. Depending on how old and dependent your dependents are (if you have children), how much money they will need to pay for college, and how much you have to lend (the amount of the loan), etc. Life insurance can usually last decades, 1 to 3 decades, depending on who you have dependents.

What factors determine Life Insurance costs in Germany?

Life insurance costs in Germany are largely determined by the amount that you are insuring, the length of the contract, and your age. There is also the death risk of the insured person at the time of the contract which plays a role in the cost of life insurance in Germany.

This means smokers might have to pay more than nonsmokers. People with a risky job may need more money for life insurance, for instance, if the job is physically demanding or the insured person has particularly risky hobbies.

You will have to pay monthly premiums as long as you determine how long your life insurance contract will last. As a rule of thumb, you should stay insured for at least as long as your children are working age (after education) and be financially independent adults or until you pay off any debts that might arise.

In essence, you should also consider staying insured as long as your family members are dependent on financial compensation.

Life insurance premiums won’t be the same as the next person’s since they are calculated according to your needs and circumstances.

The following factors affect how much you pay:

Your age when applying for a policy;

Your gender (women tend to live longer than men);

Whether or not there are other dependents who need financial support after your death;

What is your annual income;

Which Policy type (joint/single names) are you seeking;

What is your required Coverage Amount;

What is the Length of the policy;

Your health/lifestyle.

How much insurance should I take in Germany?

Newcomers to the country to work out how much insurance they should take out. Many people end up either underinsured or overinsured.

The amount of life insurance needed depends on various factors, such as how much money you make and how many dependants there are in your household.

If you have an important role in the family business or if someone else relies on their salary from working with or for you then it makes sense to take out more than just basic cover (which usually only covers funeral costs).

The amount of insurance can be determined easily with two simple strategies.

First and foremost, leave your property debt-free. Insurance would then be measured closely by the size of the outstanding mortgage debt, which decreases with time.

The second step is to specify the minimum free income you intend for your surviving partner or family to have. After that, you add up the expected income shortfall to determine the amount of insurance needed.

You usually want to cover five to 15 times your after-tax income at a time when your dependents are no longer financially dependent on you. Whether the children earn their income, or if you build up other income.

Additional features to have?

The basic protection is generally sufficient. Nevertheless, many term life insurers in Germany offer you additional features at an extra fee. Here are some examples:

If you have a serious illness and the life expectancy is less than one year, you will receive an early (full) payment of the insurance.

The insured term will be extended without a new health check.

An increase in the insurance amount in certain events, such as the birth of a child.

An occupational injury exemption from having to pay your monthly payments

Adding these components makes sense but not in all situations. Most commonly, the basic protection suffices to secure your mortgage or protect your surviving partner’s financial standing.

What are the different tariff types available?

Germany offers three different, common options for term life insurance:

Constant insurance amount

Linearly decreasing insurance amount

Annuity decreasing insurance amount

The Constant Insurance Amount can give you peace of mind and is easy to track if your monthly premium fits into your budget. Additionally, insurance is always secured in this approach.

A linearly falling insured sum means that the contributions will decrease over time. You do not need to protect your mortgage as it is decreasing and this method allows you to take this into account.

The annuity falling insurance sum can be calculated individually according to the terms of your mortgage, so the mortgage is always secured and the premium is as low as possible. This solution can also be combined with a constant insurance sum for the first few years and, for example, the insurance sum will decrease in the third year. Savings-minded individuals may be interested in this option.

Difference between tariff premium (Tarifbeitrag) and payment premium (Zahlbeitrag)

The difference between tariff premiums (Tarifbeitrag) and payment premium is that each represents the value of a life insurance contract at any time in time, and is therefore changed as circumstances change or new contracts are signed. On the other hand, the latter is fixed until either party ends it or cancels it-usually when an insured person stops paying premiums altogether or has passed away, so they don’t have any reason to remain with a provider like

What can I do if I no longer want term life insurance?

You are entitled to cancel your policy at any time. Life insurance contracts with regular premiums are normally terminated without notice by policyholders. However, the termination will only take effect after the end of the insurance period.

Usually, the earliest termination date is therefore the end of the first policy year. The insurance period is the period of time for which the premium is determined. Typically, this is one year.

Detailed conditions and consequences after terminating a policy are provided under the general insurance conditions. To avoid any negative consequences, you should read this document before terminating your policy.

Term life insurance policies where insurance premiums are paid in one lump sum are an exception. Such policies do not have a statutory right of termination. However, termination rights may be included in general insurance conditions and therefore form a part of your contract.

You will not receive reimbursements for life insurance premiums when you terminate your policy early.

Life insurance and tax obligation in Germany

As part of the German tax regime, any death penalty payout can be tax-free. A spouse can be saved from inheritance tax by making a contract on their life. It is crucial to consider this for unmarried couples as their allowance is just €20,000.

Who supervises/regulates life insurers?

The BaFin oversees German insurance companies and monitors their daily operations. As part of BaFin’s responsibilities, all insured persons are adequately protected in terms of legal and financial interests.

BaFin accepts and processes complaints about individuals’ insurance companies in order to protect their interests. However, it should be noted that BaFin cannot enforce your rights as an individual. That responsibility lies with the federal and state courts.

The quality and contents of insurance policies are not subject to review by BaFin, and BaFin cannot review insurance terms and conditions. According to the statutory requirements in the life insurance industry, insurers are generally free to decide on the design of their policies, the scope of coverage offered and the calculations that govern their policy products (contractual freedom).

In cases where baFin believes that the terms and conditions of its insurance are in breach of the law (in particular consumer protection laws) or (high) court cases, the insurer can take steps to remedy or prevent such shortcomings.

Conclusion

We hope you enjoyed this guide to the best German life insurance. If you are looking for a life insurance policy, it is important to understand that there are many different types of policies to choose from. With this in mind, we want to provide you with a few tips and pointers so that you can find the best one for yourself.

First off, make sure that you understand what German life insurance is and how it works before you start shopping around for quotes. Secondly, be sure to ask questions about each policy’s terms and conditions so that you know exactly what you’re getting into before signing on the dotted line. Finally, don’t forget about the price! You may find that one company offers better terms than another but charges more overall.